Short Questions Answer

Why is the time value of money concept so important in financial analysis?

Time value of money concept is widely applied in financial decisions. Financial decisions are carried out with the objective of maximizing value of the firm. The application of time value of money concept in financial decision making contributes toward a value maximization objective. The basic importance of the concept of time value of money are discussed below:

- Application in investment decision: One of the basic applications of the concept of time value money is widely observed in making long-term investment decisions. All long-term investment projects require spending a huge amount of capital today and with certainty. However, the benefits from the use of projects occur in small amounts over a longer period of time and with uncertainty. Thus, there is a difference in timing of cash outflows and cash inflows associated with long-term investment. Cash outflows occur at present whereas cash inflows are realized over several periods of time. Because of the timing difference, they are not directly comparable. Therefore future cash inflows are discounted back to present values to compare against the present cash outflows and make investment decisions. Long-term projects also involve risk because of the uncertainty of future cash inflows. So according to the concept of time value of money. We select an appropriate discount rate consistent to the level of risk involved in the project to calculate present values. Thus, the concept of time value of money contributes to making long-term investment decisions effectively and efficiently.

- Application in financing decision: Besides investment decisions, the concept of time value of money is also applied widely in financing decisions. Financing decision is concerned with determining optimal proportionate mix of long-term components of capital that minimizes the weighted average cost of capital. In deciding on the appropriate source of financing for the firm, we compare the effective cost of each source of financing based on the concept of time value of money.

- Application in security analysis: While analyzing the securities investment, such as investment in stock and bonds, the security analysts and investors use the concept of time value of money. In making securities investment decisions, future cash flows of securities are discounted back to present value to determine the worthiness of investment in securities.

- Application in leasing versus buying decision: Further, we use the concept of time value of money in leasing versus buying decision to calculate the present value of cost of leasing and cost of buying. The present values of costs of these two alternatives are compared against each other to decide on an appropriate source of financing.

- Other uses: Besides the above uses, the concept of time value of money is also used for other purposes as well. For example it can be used to assess the proposed credit policies and the firm’s efficiency in managing cash collections under current assets management. It can be used to plan family expenditure and investment, such as investment for safety and security as in the case of buying insurance and pension plans.

Explain what is meant by the following statement. “A rupee in hand today is worth more than a rupee to be received next year.”

Every sum of money received earlier commands a higher value than the equal sum of money received later. This statement is well explained by the concept of time value of money. The time value of money is the concept to understand the value of cash flows that occurred at different periods of time. A rupee in hand today is valued more than a rupee next year due to the following three reasons.

- Investment opportunity: Money received earlier can be invested to generate further sums of money. For example, if we receive Rs 100 today and deposit in a bank account paying 6 percent interest, we will have Rs 106 at the end of the year. Therefore, given this investment opportunity Rs 100 today is equivalent to Rs 106 at the end of year.

- Preference toward current consumption: Most people prefer current consumption to future consumption. Money in hand today makes current consumption possible. Therefore, Current sum of money is more valuable.

- Inflation: A sum of money today is worth more than the equal sum of money a year later due to inflation. Inflation kills purchasing power of the money. If the rate of inflation is 5 percent, we need Rs 105 to buy a basket of commodities a year later than what we could buy with Rs 100 today.

Write Short Notes on:

Time value of money

The time value of money is the concept to understand the value of cash flows that occurred at different periods of time. Every sum of money received earlier commands a higher value than the equal sum of money received later. This statement is well explained by the concept of time value of money. A rupee in hand today is valued more than a rupee next year due to the fact that money received earlier can be invested to generate further sums of money. For example, if we receive Rs 100 today and deposit in a bank account paying 6 percent interest, we will have Rs 106 at the end of the year. Therefore, given this investment opportunity Rs 100 today is equivalent to Rs 106 at the end of year. Current money in hand is also important because it allows current consumption. Further, in the inflationary environment, a present sum of money has higher purchasing power than the equal sum of money in future.

Time value of money concept is widely applied in financial decisions. One basic application of the concept of time value money is widely observed in making long-term investment decisions. In all long-term investment decisions, future cash inflows are discounted back to present values to compare against the present cash outflows. Further, the concept of time value of money is also applied widely in financing decisions to compare the effective cost of each source of financing. Besides, while analyzing the securities investment, such as investment in stock and bonds, the security analysts and investors use the concept of time value of money to discount the future cash flows back to present value to determine the worthiness of investment in securities. It can also be used to plan family expenditure and investment, such as investment for safety and security as in the case of buying insurance and pension plans.

Amortized loans

Amortized loans are those loans that are repaid in equal periodic installments over a loan contract period. The equal periodic installments contain both- a part of principal repayment and the interest payment on outstanding loan. This type of loan is more common on hire purchase financing of autos and home appliances in Nepal. Besides, commercial banks in Nepal also extend housing loans for a longer period of time which are repaid in equal monthly installments (EMI). In amortized loans, the equal periodic installment is called ‘Payment’. It is determined on the basis of the concept of time value of money. A payment is a series of equal future payments on the loan that has a total present value equal to the amount of loan at a given interest rate. It is worked out as follows:

Payment (PMT)= PVIFA ;%n year /Amount of Loan

Once the equal payment is worked out using the above relation, we prepare an amortization schedule. An amortization schedule is the schedule of loan repayment which shows in detail the payment made each period including interest payment and a part of principal repayment. The interest payment each period declines and the part of principal repayment each period increases without affecting the installment. In other words, the proportion of interest on each payment declines every period while the proportion of principal repayment each period increases.

Numerical Problems:

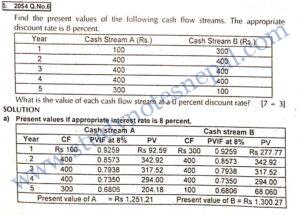

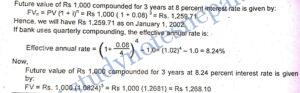

Assume that it is now January 1, 1998. In January 1999, you will deposit Rs. 1,000 into a savings account that pays 8%. If the bank compounds interest annually, how much will you have in your account on January 1, 2002? What would your January 1, 2002, balance be if the bank used quarterly compounding rather than annual compounding?

Assume that it is now January 1, 1998. In January 1999, you will deposit Rs. 1,000 into a savings account that pays 8%. If the bank compounds interest annually, how much will you have in your account on January 1, 2002? What would your January 1, 2002, balance be if the bank used quarterly compounding rather than annual compounding?

SOLUTION

Annual payment (PMT) = Rs 60,000 per year

Interest rate (i) = 8%

n= 4 years

The amount that must be deposited today is given by:

PVAn= PMT x PVIFA i,n= Rs 60,000 x PVIFA 8%, 4 = Rs 60,000 x 3.3121 = Rs 198,726

Assume that it is now January 1, 1998, and you will need Rs. 1000 on January 1, 2002. Your bank compounds interest at an 8% rate annually.

(a) How much must you deposit on January 1, 1999 to have a balance of 1,000 on January 1, 2002?

(b) if you want to make equal payments on each January 1 from 1999 through 2002 to accumulate the Rs. 1000, how large must each of the four payments be?

(c) If your father were to offer either to make the payments calculated in Part B or to give you a lump sum of Rs. 750 on January 1, 1999, which would you choose?

(d) If you have only Rs. 750 on January 1, 1999, what interest rate, compounded annually, would you have to earn to have the necessary Rs.1000 on January 1, 2002?

Assume that it is now January 1, 1998, and you will need Rs. 1000 on January 1, 2002. Your bank compounds interest at an 8% rate annually.

(a) How much must you deposit on January 1, 1999 to have a balance of 1,000 on January 1, 2002?

(b) if you want to make equal payments on each January 1 from 1999 through 2002 to accumulate the Rs. 1000, how large must each of the four payments be?

(c) If your father were to offer either to make the payments calculated in Part B or to give you a lump sum of Rs. 750 on January 1, 1999, which would you choose?

(d) If you have only Rs. 750 on January 1, 1999, what interest rate, compounded annually, would you have to earn to have the necessary Rs.1000 on January 1, 2002?

- What is the present value of a security that promises to pay you Rs. 5,000 in 20 years? Assume that you can earn 7 percent if you were to invest in other securities of equal risk.

- You are thinking about buying a car, and a local bank is willing to lend you Rs. 20,000 to buy the car. Under the terms of the loan, it will be fully amortized over 5 years (60 months), and the nominal rate of interest will be 12 percent, with interest paid monthly, what would be the monthly payment on the loan? What would be the effective rate of interest on the loan?

Why is the time value of money concept so important in financial analysis?

Time value of money concept is widely applied in financial decisions. Financial decisions are carried out with the objective of maximizing value of the firm. The application of time value of money concept in financial decision making contributes toward a value maximization objective. The basic importance of the concept of time value of money are discussed below:

- Application in investment decision: One of the basic applications of the concept of time value money is widely observed in making long-term investment decisions. All long-term investment projects require spending a huge amount of capital today and with certainty. However, the benefits from the use of projects occur in small amounts over a longer period of time and with uncertainty. Thus, there is a difference in timing of cash outflows and cash inflows associated with long-term investment. Cash outflows occur at present whereas cash inflows are realized over several periods of time. Because of the timing difference, they are not directly comparable. Therefore future cash inflows are discounted back to present values to compare against the present cash outflows and make investment decisions. Long-term projects also involve risk because of the uncertainty of future cash inflows. So according to the concept of time value of money. We select an appropriate discount rate consistent with the level of risk involved in the project to calculate present values. Thus, the concept of time value of money contributes to making long-term investment decisions effectively and efficiently.

- Application in financing decision: Besides investment decisions, the concept of time value of money is also applied widely in financing decisions. Financing decision is concerned with determining optimal proportionate mix of long-term components of capital that minimizes the weighted average cost of capital. In deciding on the appropriate source of financing for the firm, we compare the effective cost of each source of financing based on the concept of time value of money.

- Application in security analysis: While analyzing the securities investment, such as investment in stock and bonds, the security analysts and investors use the concept of time value of money. In making securities investment decisions, future cash flows of securities are discounted back to present value to determine the worthiness of investment in securities.

- Application in leasing versus buying decision: Further, we use the concept of time value of money in leasing versus buying decision to calculate the present value of cost of leasing and cost of buying. The present values of costs of these two alternatives are compared against each other to decide on an appropriate source of financing.

- Other uses: Besides the above uses, the concept of time value of money is also used for other purposes as well. For example it can be used to assess the proposed credit policies and the firm’s efficiency in managing cash collections under current assets management. It can be used to plan family expenditure and investment, such as investment for safety and security as in the case of buying insurance and pension plans.

What is the present value of a security that promises to pay you Rs. 5,000 in 20 years? Assume that you can earn 7 percent if you were to invest in other securities of equal risk.

- You are thinking about buying a car, and a local bank is willing to lend you Rs. 20,000 to buy the car. Under the terms of the loan, it will be fully amortized over 5

Thank you very much for uploading the informative content. It helped me a lot solving the financial problems.